If you’re a retiree looking for safe, steady income from your investments, you probably know the usual suspects: dividend-paying utilities, blue-chip stocks, or maybe a solid bond ladder. But there’s one income-producing stock that deserves a place in every retirement portfolio—yet is often overlooked by everyday investors.

That stock is Brookfield Asset Management (BAM). And in today’s world of rising inflation, infrastructure spending, and a growing need for dependable income, Brookfield is built to thrive.

In this post, I’ll show you why BAM is not only a smart income investment—but arguably the best dividend stock in the entire financial sector.

Why Brookfield Is Different

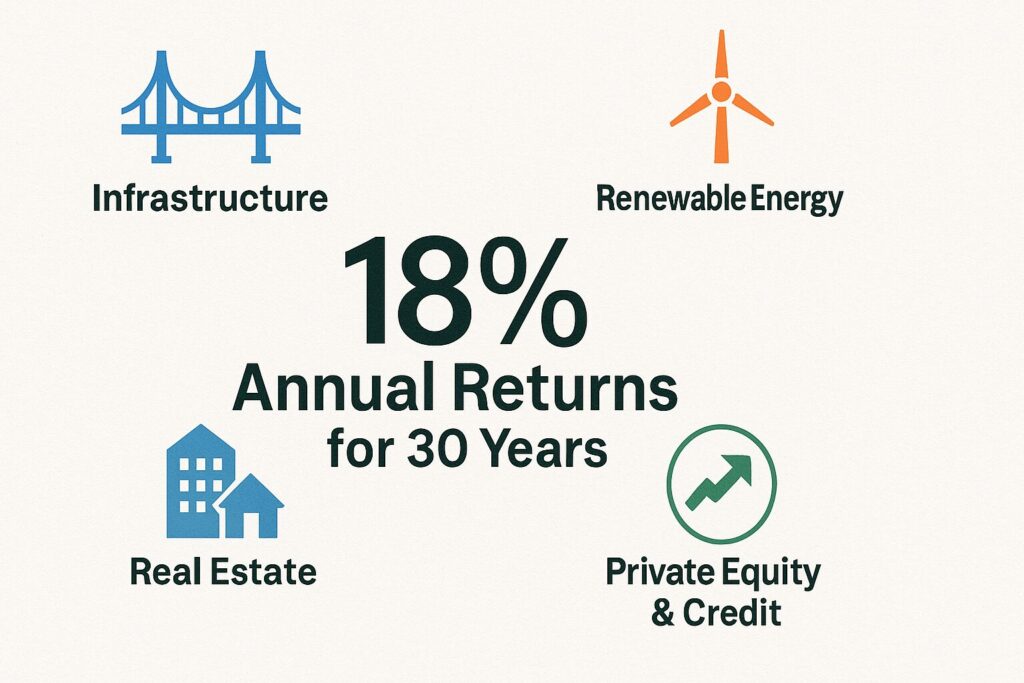

Brookfield Asset Management isn’t your typical Wall Street firm. It doesn’t make its money from trading or speculation. Instead, BAM makes steady, predictable income by managing real assets like infrastructure, renewable energy, private credit, and real estate.

It focuses on long-term contracts with built-in inflation protection, and then shares most of its profits with shareholders through a rising dividend.

That’s the kind of business retirees should love: real cash flow from real assets, distributed as real income.

Three Big Trends Driving Brookfield’s Growth

Brookfield sits at the center of three unstoppable global trends that will define the next decade:

1. The Global Energy Transition

Governments around the world are racing to shift from fossil fuels to renewable energy. That means massive investment in solar, wind, hydro, and battery storage—the exact kinds of projects Brookfield specializes in. With its decades of experience, Brookfield is a trusted partner for both governments and private capital.

2. AI-Powered Infrastructure

Artificial intelligence isn’t just software. It requires huge physical infrastructure—from data centers and fiber optic cables to next-generation power grids. Brookfield is already investing billions in these “behind the scenes” assets, and the demand is only growing.

3. The Rise of Private Credit

As traditional banks pull back, institutional investors are pouring money into private credit. Brookfield lends directly to businesses—mostly with secured, low-risk loans—and earns stable interest income in return. This market is booming, and BAM is one of its top players.

Brookfield’s Secret Sauce: Fee-Based Income with Inflation Protection

At its core, Brookfield is a fee-based business. It raises money from pension funds, sovereign wealth funds, and insurers. Then it invests that capital in long-term, income-generating projects. In return, Brookfield collects a percentage of those assets under management (AUM)—year after year.

Here’s what makes that model perfect for retirees:

- The fees are recurring. No one-off hits or unpredictable profits.

- The contracts are long-term. Many last 10 years or more.

- Most deals have inflation-linked escalators. That means as the cost of living rises, Brookfield’s income goes up too—and so can your dividend.

In short, BAM is built for long-term, inflation-resistant income.

Show Me the Money: Dividends You Can Count On

Let’s talk numbers.

Brookfield pays out more than 90% of its earnings to shareholders. That’s music to an income investor’s ears.

And unlike many finance stocks, BAM’s dividend doesn’t bounce around based on quarterly profits. It’s a fixed, steadily rising dividend, backed by recurring fees—not market timing or risky bets.

Here’s what the recent history looks like:

- In 2024, BAM raised its quarterly dividend from $0.32 to $0.38.

- In 2025, it raised it again to $0.44—a 15% increase.

- Management has projected that earnings will double by 2028, meaning the dividend could double too.

Right now, Brookfield yields about 3.5% to 4%, depending on the price you pay. That’s already better than most banks or utilities—and it’s likely to grow significantly.

This is income with a built-in escalator.

Why BAM Beats the Other Big Names

You’ve probably heard of BlackRock (BLK), Blackstone (BX), Apollo (APO), or KKR. They’re all giant asset managers. But when it comes to retiree-friendly dividends, Brookfield stands above the rest.

Here’s why:

- BlackRock dominates passive ETFs, but its dividend is smaller and its business is more tied to market moves.

- Blackstone pays a dividend based on performance fees, which can be very inconsistent.

- Apollo has a heavy insurance exposure that makes its financials more complex.

- KKR is a solid operator but reinvests more and pays a lower dividend.

Brookfield, in contrast, offers:

✅ A clear and growing dividend,

✅ Fee-based income that’s recurring and predictable,

✅ Exposure to real assets that do well in inflationary environments, and

✅ A clean corporate structure (no confusing K-1 tax forms, just a regular 1099).

It’s the financial sector’s most retiree-friendly dividend stock.

Brookfield’s Moat: Built to Last

Brookfield didn’t just show up yesterday. It’s been building this empire for decades. Its success comes from a wide, deep economic moat that competitors find hard to cross.

Some key strengths:

- Global reach: 30+ countries, with over 1,300 investment professionals.

- Vertical integration: It builds, finances, operates, and monetizes its own assets.

- Strong partnerships: From government agencies to sovereign wealth funds, Brookfield is often the first call when there’s a $10B infrastructure deal on the table.

- Skin in the game: Brookfield invests in its own deals. Its managers and insiders have their own capital tied up right alongside investors—just how it should be.

Brookfield’s structure makes it more than just an asset manager. It’s a compounding machine that turns capital into long-term income streams—and then shares those streams with shareholders.

What About Risks?

No investment is risk-free. But BAM is one of the most durable dividend payers out there. Here are some common concerns—and why they’re manageable:

✅ Interest Rates Stay Higher for Longer?

No problem. Brookfield’s contracts often adjust with inflation, and most of its projects are structured to work even in higher-rate environments.

✅ Private Credit Blowups?

Brookfield plays it safe. It sticks to senior, secured loans and avoids the riskiest parts of the market.

✅ Fundraising Slows?

Even in volatile markets, Brookfield has continued raising capital. Institutions trust them—and that trust isn’t going away.

In short, BAM is built to weather the storm. Its business model is designed for resilience, even in uncertain markets.

The Road Ahead: Your Retirement Ally

Brookfield isn’t flashy. It doesn’t make headlines every week. But that’s what makes it so appealing.

While other companies chase trends, BAM is already positioned at the center of the biggest, most durable shifts in the global economy:

- AI’s insatiable demand for data infrastructure

- The electrification of transportation

- Renewable energy buildouts

- Institutional hunger for yield in a low-growth world

And all the while, it quietly sends more income to shareholders, year after year.

The Final Word: Your Anchor Stock for the Decade Ahead

If you’re a retiree building a dividend portfolio to last the next 10 or 20 years, Brookfield Asset Management deserves a top spot.

It’s the kind of company that:

- Provides stable, inflation-protected income

- Offers strong dividend growth

- Has a global, institutional-grade business model

- Is aligned with the biggest trends of the next decade

You may not hear about BAM on CNBC every night—but that’s exactly why it works. It’s a stock you can buy and hold, knowing it’s built to compound quietly in the background while you enjoy retirement.

Bottom line? Brookfield doesn’t just manage assets. It builds wealth—and it shares that wealth with shareholders.

For retirees who want to take a closer look at Brookfield and understand why it stands out as a premier income investment, my book The Single Best Dividend Stock for Retirees offers a detailed, easy-to-follow deep dive into the company’s business model, dividend strategy, and long-term growth potential. It’s available now on Amazon.com in both paperback and eBook format.

Disclosure: This article is for informational purposes only and is not a recommendation to buy or sell any security. Always do your own research or consult a financial advisor to ensure any investment is appropriate for your financial situation.