Smarter Withdrawals, Lower Taxes, and a Bigger Retirement Paycheck

One of the biggest surprises for many retirees is that retirement doesn’t automatically mean lower taxes. In fact, if you’re not careful, your withdrawals from IRAs, pensions, and Social Security could push you into a higher tax bracket—and cost you thousands more than necessary.

The good news? You can take control. With a smart withdrawal strategy, you can stay in a lower tax bracket, reduce your overall tax burden, and make your money last longer.

🎯 Why Your Tax Bracket Matters in Retirement

In retirement, you’re likely drawing income from several sources:

- Social Security

- Traditional IRAs or 401(k)s (taxable)

- Roth IRAs (tax-free)

- Pensions or annuities

- Dividends and interest

- Part-time work

Each source can affect your tax bracket—and how much of your income is taxed.

If you withdraw too much from a taxable source in one year, you could:

- Push part of your Social Security into taxable territory

- Pay a higher marginal rate on your IRA withdrawals

- Trigger higher Medicare premiums (called IRMAA)

- Lose eligibility for certain tax credits or deductions

Strategic withdrawals = smaller tax bills.

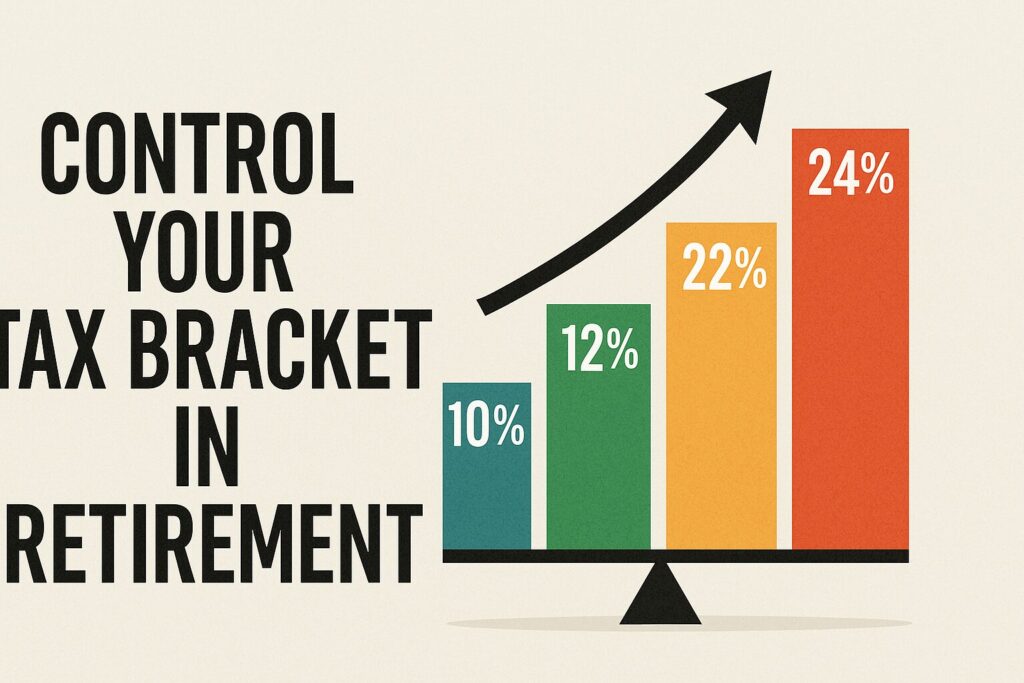

📘 What Are the Federal Tax Brackets?

For 2025 (estimated figures based on inflation), here are the married filing jointly tax brackets:

- 10%: $0 – $22,000

- 12%: $22,001 – $89,450

- 22%: $89,451 – $190,750

- 24%: $190,751 – $364,200

- And so on…

Single filers fall into the next bracket sooner.

Your marginal tax rate is the rate you pay on your last dollar of income. The goal is to stay in a lower bracket as much as possible.

🧠 Smart Strategies to Stay in the Right Bracket

1. Use Roth Withdrawals Strategically

If you have a Roth IRA, consider using tax-free withdrawals to supplement income and stay under key thresholds.

Example: If you’re in the 12% bracket and nearing the 22% cutoff, switch to Roth withdrawals to avoid jumping into the next bracket.

2. Take Required Minimum Distributions (RMDs) Wisely

Once you hit age 73, the IRS requires you to withdraw a minimum amount from traditional IRAs and 401(k)s.

But you don’t have to take all your income from your RMD. Balance it with:

- Roth withdrawals

- Taxable brokerage accounts (long-term gains may be taxed at 0%)

- Social Security (more on that below)

Plan ahead to avoid large RMDs that spike your tax rate later in life.

3. Delay Social Security if You Can

Delaying Social Security until age 70:

- Increases your benefit

- Gives you a chance to draw down your IRA/401(k) before RMDs

- Helps control taxes early in retirement

Plus, fewer income sources early on makes it easier to fill the 10% or 12% bracket with strategic IRA withdrawals.

4. Fill Up the Lower Brackets Early

If you’re in the 10% or 12% tax bracket, consider taking larger IRA withdrawals or doing Roth conversions—intentionally.

Why? You’re paying taxes at a low rate now, possibly lower than what you’ll pay later when RMDs and Social Security kick in.

Tip: Work with a tax professional to “fill up” your bracket efficiently each year.

5. Beware of the Medicare Cliff

If your income exceeds certain thresholds, your Medicare premiums go up—significantly.

For 2025, the IRMAA thresholds for a single filer are:

- Over $103,000 = higher Medicare Part B & D premiums

- Over $206,000 = even higher premiums

Keep an eye on Modified Adjusted Gross Income (MAGI) when making withdrawals to avoid these costly jumps.

💡 A Real-Life Example

Meet Sam and Linda, both age 70 and retired.

They have:

- $800,000 in a traditional IRA

- $100,000 in a Roth IRA

- $30,000 in a savings account

- $50,000/year in Social Security benefits

They need about $70,000 a year to live on.

Instead of taking it all from the IRA (which would trigger a 22% tax bracket and make 85% of their Social Security taxable), they:

- Take just $35,000 from the IRA

- Use $15,000 from their savings

- Withdraw $20,000 from the Roth (tax-free)

Their taxable income stays within the 12% bracket, and only part of their Social Security is taxed. By mixing and matching, they avoid higher taxes and make their money last longer.

🧾 Bonus Tip: Use Tax Software or a Planner

Taxes in retirement can get complex. A small misstep can cost you big—so using retirement tax planning software or working with a CPA or financial planner can pay for itself many times over.

Many professionals offer retirement income planning sessions to help you see:

- Your projected tax bracket

- When to take what from each account

- Opportunities to reduce lifetime taxes

✅ Quick Recap

To control your tax bracket in retirement:

- Use Roth accounts to stay under bracket thresholds

- Take IRA withdrawals early while you’re in a low bracket

- Delay Social Security when it makes sense

- Be strategic with Required Minimum Distributions

- Watch your Medicare income limits

- Consider small Roth conversions in low-income years

These strategies may seem small—but over a 25-year retirement, they can save you tens of thousands in unnecessary taxes.

📘 This post is adapted from my book:

Tax Loopholes Just for Seniors: 33 Ways to Slash Your Taxes Right Now

Available now at Amazon.com in paperback and eBook formats.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Everyone’s situation is different. Please consult a qualified tax professional before making decisions based on this information.