Why Playing It Too Safe Can Quietly Erode Your Financial Security in Retirement

Welcome to “Money Myths Retirees Still Believe”—a blog series that uncovers the hidden beliefs that can quietly sabotage your financial peace of mind.

Many retirees cling to common money myths that seem true but can lead to poor decisions, lost income, or unnecessary worry. Each post in this series explores one myth—like “cash is trash” or “I need to beat the market”—and replaces it with a smarter, simpler mindset.

If you’re retired or nearing retirement, this series will help you reassess your approach and feel more confident about your financial future.

The Myth: “I’m Being Careful—That’s Why I Don’t Invest”

Ed, a 74-year-old retired postal worker, proudly told his friends he’d pulled all his money from the stock market. “It’s too risky,” he said. “I’m just being careful. CDs and savings accounts are all I need.”

But over time, Ed noticed something troubling.

His income wasn’t keeping up with his expenses.

The prices at the grocery store kept rising.

And his savings weren’t growing—at all.

Ed thought he was playing it safe.

But he had unknowingly fallen into a different kind of risk—the slow, silent risk of losing ground to inflation.

Why This Myth Feels True

It’s perfectly natural to want to protect what you’ve worked hard for.

After all, you’re retired now. You don’t want drama. You don’t want to gamble.

So, keeping everything in cash, CDs, or money market accounts feels safe.

But over time, the cost of living goes up. And if your money isn’t growing, it’s actually shrinking in purchasing power—even if the balance stays the same.

This is the trap of being “too safe.”

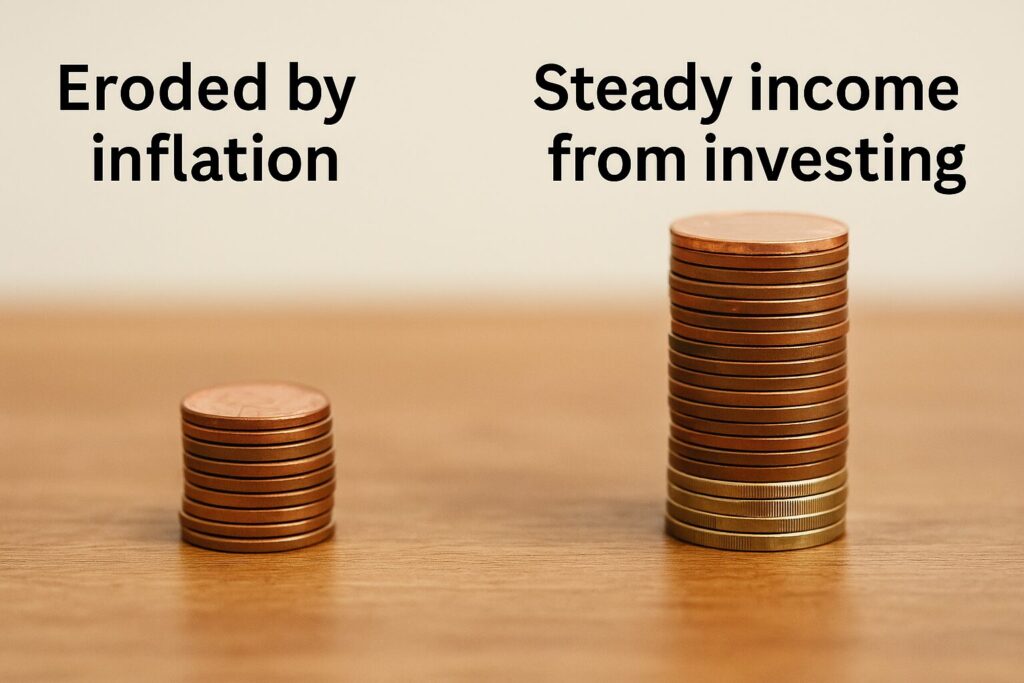

The Real Risk of Being Ultra-Conservative

Let’s say you have $100,000 sitting in a savings account earning 1%.

Inflation is running at 3%. That means every year, you’re losing about 2% in purchasing power.

In 10 years, your $100,000 might only buy what $82,000 buys today.

In 20 years? More like $67,000.

You didn’t lose it in the market—you lost it by standing still.

The Smarter Mindset: Be Protective, Not Paralyzed

You don’t have to swing for the fences. You don’t need risky growth stocks or volatile crypto funds.

But you do need a plan that includes moderate, thoughtful investing—enough to keep your income steady and your money ahead of inflation.

Here’s what that can look like:

✅ Dividend Income Funds

These can provide 3–5% in regular income with less risk than individual stocks.

✅ Bond Ladders

Staggered maturities (1-year, 2-year, etc.) provide predictable income and help manage interest rate risk.

✅ REITs and Income ETFs

Real estate and other income-producing investments can offer steady monthly or quarterly payouts.

✅ Balanced Portfolios

Mix conservative stock funds and bonds to create growth and income with less volatility.

✅ Cash for Short-Term Needs

Hold 6–12 months of living expenses in cash—but don’t let the rest sit idle.

A Real-Life Example

Patricia, a 68-year-old retired librarian, kept all her savings in CDs for years. But after watching her fixed income lose value to rising living costs, she decided to invest just 40% of her savings into a conservative dividend ETF and a municipal bond fund.

The result?

Her income went up. Her taxes stayed low. And she didn’t lose sleep—because she still had cash on hand for emergencies.

“I used to think investing was risky,” she said. “Now I see that not investing was the real risk.”

3 Questions to Ask Yourself

- Is my income growing or staying flat?

- Am I beating inflation—or falling behind?

- If I live 25 more years, will my money keep up with me?

If you’re not sure, it may be time to revisit your plan.

The Takeaway

It’s wise to be cautious. But being too cautious can quietly erode your financial security.

You don’t need to be aggressive.

You just need to be intentional.

Keep enough cash for the short-term, and let the rest of your money work for you—not gather dust.

Because in retirement, safety doesn’t mean hiding your money.

It means protecting your future—and that includes smart, steady investing.