When most people hear the words “life insurance,” they think of one thing: a payout to their loved ones after they pass away.

But what if I told you that certain types of life insurance—specifically cash value life insurance—can also help you build wealth, grow your savings tax-deferred, and even provide income during retirement?

For retirees or soon-to-be retirees looking for safe, stable financial strategies, cash value life insurance may be one of the best-kept secrets in the retirement planning world.

Let’s take a closer look at how it works, why it’s so powerful, and how real-life retirees are using it to live better, stress less, and pass on more to the next generation.

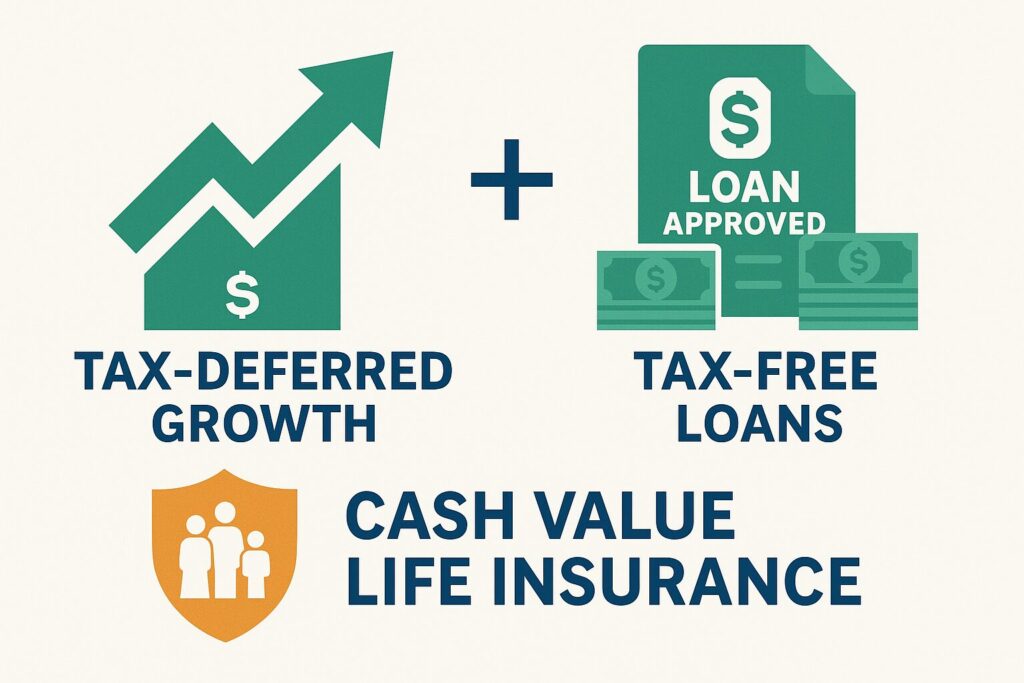

What Is Cash Value Life Insurance?

Cash value life insurance is a type of permanent life insurance, which includes policies like whole life, universal life, and indexed universal life. Unlike term life insurance (which expires after a set number of years and has no value unless you die during the term), cash value policies last your entire life—and build a growing savings account along the way.

Here’s what makes it different:

- Part of your premium goes toward the death benefit

- Another part goes into a cash value account

- That account grows over time, tax-deferred

Think of it like a hybrid between insurance and a savings account—with powerful tax advantages and long-term financial benefits.

The Power of Tax-Deferred Growth

One of the biggest benefits of cash value life insurance is that the money in your cash value account grows tax-deferred. That means you won’t pay taxes on the growth as long as it stays in the policy.

Compare that to a taxable investment account, where Uncle Sam takes a bite every year from your interest, dividends, or capital gains.

Better yet, when you structure the policy properly, you can access the money tax-free through policy loans or withdrawals—while still keeping your life insurance in place.

In essence, it’s like having your own personal bank that:

- Earns steady growth

- Avoids annual taxes

- Lets you borrow or withdraw when needed

- Pays your family a tax-free death benefit someday

Real-Life Example: How Mike Used Cash Value to Retire Early

Mike, 62, had been putting money into a cash value life insurance policy for over 20 years. While his friends focused on 401(k)s and IRAs, Mike liked the idea of having safe money he could tap into without worrying about stock market crashes or required minimum distributions.

By the time he retired, Mike had built up over $150,000 in his cash value account. Instead of drawing down his retirement accounts during a market downturn, he borrowed $30,000 from his life insurance cash value to help cover expenses for a few years. No taxes. No penalties. No paperwork.

Today, Mike still enjoys the peace of mind that comes from knowing he has a backup source of income—and a tax-free death benefit his wife will receive someday.

Why Retirees Love This Strategy

There are a lot of reasons why retirees (and near-retirees) are turning to cash value life insurance as part of their financial plan:

✅ Guaranteed Growth

Many cash value policies come with minimum guarantees. You don’t have to worry about losing money in a bear market. The value goes up steadily, year after year.

✅ Tax-Free Loans

Need access to cash? You can borrow against your policy’s value without triggering taxes. Unlike 401(k) withdrawals, there are no age limits or required minimum distributions.

✅ Flexible Income

You can use policy loans as a tax-free income stream in retirement, which may help reduce your taxable income and avoid higher Medicare premiums or taxes on Social Security.

✅ Legacy Planning

The tax-free death benefit makes it easy to pass on wealth to your spouse, children, or grandchildren. It’s a simple, efficient estate planning tool—no probate, no delays.

✅ Asset Protection

In many states, the cash value inside a life insurance policy is protected from creditors—a unique benefit for retirees who want to preserve wealth and avoid legal risks.

How Cash Value Life Insurance Compares to Other Retirement Tools

| Feature | 401(k)/IRA | Cash Value Life Insurance |

|---|---|---|

| Tax-deferred growth | ✅ | ✅ |

| Tax-free withdrawals | ❌ (mostly taxable) | ✅ (loans and some withdrawals) |

| Required minimum distributions | ✅ at age 73 | ❌ |

| Market risk | ✅ | ❌ (guaranteed or stable growth) |

| Income during market crashes | Risky | Stable |

| Death benefit | ❌ | ✅ (tax-free) |

As you can see, life insurance doesn’t replace your 401(k) or IRA—it complements them. It’s a way to diversify your retirement strategy with safe money that won’t vanish during a recession.

Real-Life Example: How Carol Avoided a Tax Bomb

Carol, 70, had done a great job saving. Her IRA had grown to nearly $700,000. But when her required minimum distributions kicked in at age 73, she realized those withdrawals would push her into a higher tax bracket and raise her Medicare premiums.

Fortunately, she’d started a small whole life policy years ago. With over $50,000 in cash value, she began borrowing $10,000 a year to supplement her income—instead of taking more from her IRA.

The result? Lower taxes. Lower Medicare costs. And a smoother retirement.

Is It Right for You?

Cash value life insurance isn’t for everyone. It works best if:

- You can afford to fund the policy for several years

- You’re looking for tax-deferred growth and tax-free income

- You want long-term peace of mind and flexibility

- You value both income and legacy planning

It’s especially powerful for people in or near retirement who want to:

- Reduce taxable income

- Avoid required minimum distributions

- Leave money to heirs tax-free

- Have a source of income that’s not tied to the stock market

And here’s a bonus: If you set up a policy early enough, you can even use it to pay for long-term care or medical expenses in later years—without draining your savings.

Final Thoughts: A Proven Strategy That’s Been Hiding in Plain Sight

Cash value life insurance has been used by savvy investors, business owners, and even banks for decades to build wealth safely and predictably. But most everyday retirees still think it’s just about death benefits.

It’s time to change that.

When structured correctly, cash value life insurance can be:

- A safe, tax-deferred savings vehicle

- A source of retirement income

- A tool to reduce taxes and preserve wealth

- A legacy plan for your loved ones

It’s not a magic bullet—but it is a powerful tool to consider as part of a well-rounded retirement plan.

Want to Learn More?

This article is adapted from my book, The Life Insurance Secret: How to Grow Rich Using Cash Value Life Insurance, available now on Amazon.com in both paperback and eBook formats.

You’ll learn how real people use these policies to boost their retirement income, protect their families, and enjoy more peace of mind—without taking big risks.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consult with a qualified advisor before making insurance or investment decisions.